Hey there, future college student! As you prepare for your higher education journey, one important aspect to consider is how you will finance your studies. Student loans can be a helpful tool in covering the cost of tuition, books, and living expenses. However, navigating the world of student loans can be overwhelming. In this guide, we will walk you through the process of shopping for student loans, exploring your options, and finding the best fit for your needs. Let’s dive in and make the process easier for you!

Understanding the Different Types of Student Loans

When it comes to financing your education, student loans can be a great option to help cover the costs of tuition, books, and living expenses. However, navigating the world of student loans can be overwhelming, as there are many different types to choose from. Understanding the different types of student loans available to you can help you make an informed decision about which option is best for your individual needs. Here, we will break down the most common types of student loans to help you make sense of your options.

Federal student loans are loans that are funded by the government and offer benefits such as fixed interest rates and flexible repayment plans. There are two main types of federal student loans: Direct Subsidized Loans and Direct Unsubsidized Loans. Direct Subsidized Loans are available to undergraduate students who demonstrate financial need, and the government pays the interest on these loans while the student is in school. Direct Unsubsidized Loans are available to both undergraduate and graduate students, regardless of financial need, but interest accrues on these loans from the time they are disbursed. Additionally, there are Direct PLUS Loans, which are available to graduate students and parents of dependent undergraduate students to help cover educational expenses not covered by other financial aid.

Private student loans, on the other hand, are loans that are offered by banks, credit unions, and other private lenders. These loans often have variable interest rates and less flexible repayment options than federal student loans. However, private student loans can be a good option for students who have exhausted their federal loan options and still need additional funding for their education. It’s important to shop around and compare interest rates and terms from multiple lenders to ensure you are getting the best deal on a private student loan.

Another type of student loan to consider is a Parent PLUS Loan, which is a federal loan available to parents of dependent undergraduate students. These loans can help fill the gap between the cost of attendance and other financial aid received by the student. Parent PLUS Loans have fixed interest rates and flexible repayment options, making them a popular choice for parents looking to help their children finance their education.

Understanding the different types of student loans available to you can help you make an informed decision about how to finance your education. Whether you choose a federal student loan, a private student loan, or a Parent PLUS Loan, it’s important to carefully consider the terms and conditions of each loan before making a decision. By doing your research and comparing your options, you can ensure that you are choosing the best loan for your individual needs and circumstances.

Comparing Interest Rates and Terms for Student Loans

When shopping for student loans, it is important to carefully compare the interest rates and terms offered by different lenders. Interest rates can have a significant impact on the total cost of your loan over time, so it is crucial to choose a loan with a competitive rate. Additionally, the terms of the loan, such as the length of the repayment period and any available repayment options, can also play a role in determining which loan is the best fit for your financial situation.

One of the first things to consider when comparing interest rates for student loans is whether the rate is fixed or variable. Fixed interest rates remain the same for the entire term of the loan, providing borrowers with a sense of stability and predictability in their monthly payments. On the other hand, variable interest rates can fluctuate over time, potentially leading to higher or lower payments depending on market conditions. It’s important to weigh the benefits of a fixed rate, such as consistency, against the potential savings of a variable rate.

In addition to the interest rate itself, borrowers should also pay attention to any fees associated with the loan. Some lenders may charge origination fees, late payment fees, or prepayment penalties that can add to the overall cost of the loan. Be sure to factor in these extra costs when comparing loan offers to get a true picture of the total expense.

When evaluating the terms of student loans, consider the length of the repayment period and any available options for repayment. A longer repayment period can lead to lower monthly payments but may result in paying more interest over time. Conversely, a shorter repayment period can lead to higher payments but can help you save on interest in the long run. Additionally, look for loans that offer flexible repayment options, such as income-driven repayment plans or forbearance options, which can provide relief if you experience financial hardship.

Finally, don’t forget to consider the reputation and customer service of the lender when comparing student loan options. Look for reviews from other borrowers to get a sense of how the lender treats its customers and handles any issues that may arise. A lender with a good track record of customer satisfaction is more likely to provide a positive experience throughout the life of your loan.

Determining Eligibility Requirements for Student Loans

When shopping for student loans, it is important to understand the eligibility requirements that lenders have in place. These requirements vary depending on the type of loan you are applying for, but there are some common factors that most lenders will consider.

One of the main factors that lenders look at is your credit history. This includes your credit score, which is a numerical representation of your creditworthiness. If you have a high credit score, you are more likely to be approved for a loan and may qualify for lower interest rates. On the other hand, if you have a low credit score, you may have trouble getting approved for a loan or may be required to pay higher interest rates.

Another key factor that lenders consider is your income. Lenders want to make sure that you have the means to repay the loan, so they will typically ask for proof of income. This can include pay stubs, tax returns, or other documents that show how much money you make. If your income is too low, you may not be approved for a loan, or you may be offered a smaller loan amount.

In addition to credit history and income, lenders will also look at your enrollment status and academic progress. Most student loans require that you be enrolled at least half-time in a degree-granting program. Some lenders may also have GPA requirements, so it is important to maintain good academic standing in order to qualify for certain loans.

Finally, some lenders may have specific requirements based on your citizenship status or residency. For example, international students may have to provide additional documentation to prove that they are eligible for a loan in the United States. Additionally, some lenders may only offer loans to students who are U.S. citizens or permanent residents.

Overall, it is important to carefully review the eligibility requirements for each loan you are considering before applying. By understanding what lenders are looking for, you can increase your chances of being approved for a loan and securing the financing you need for your education.

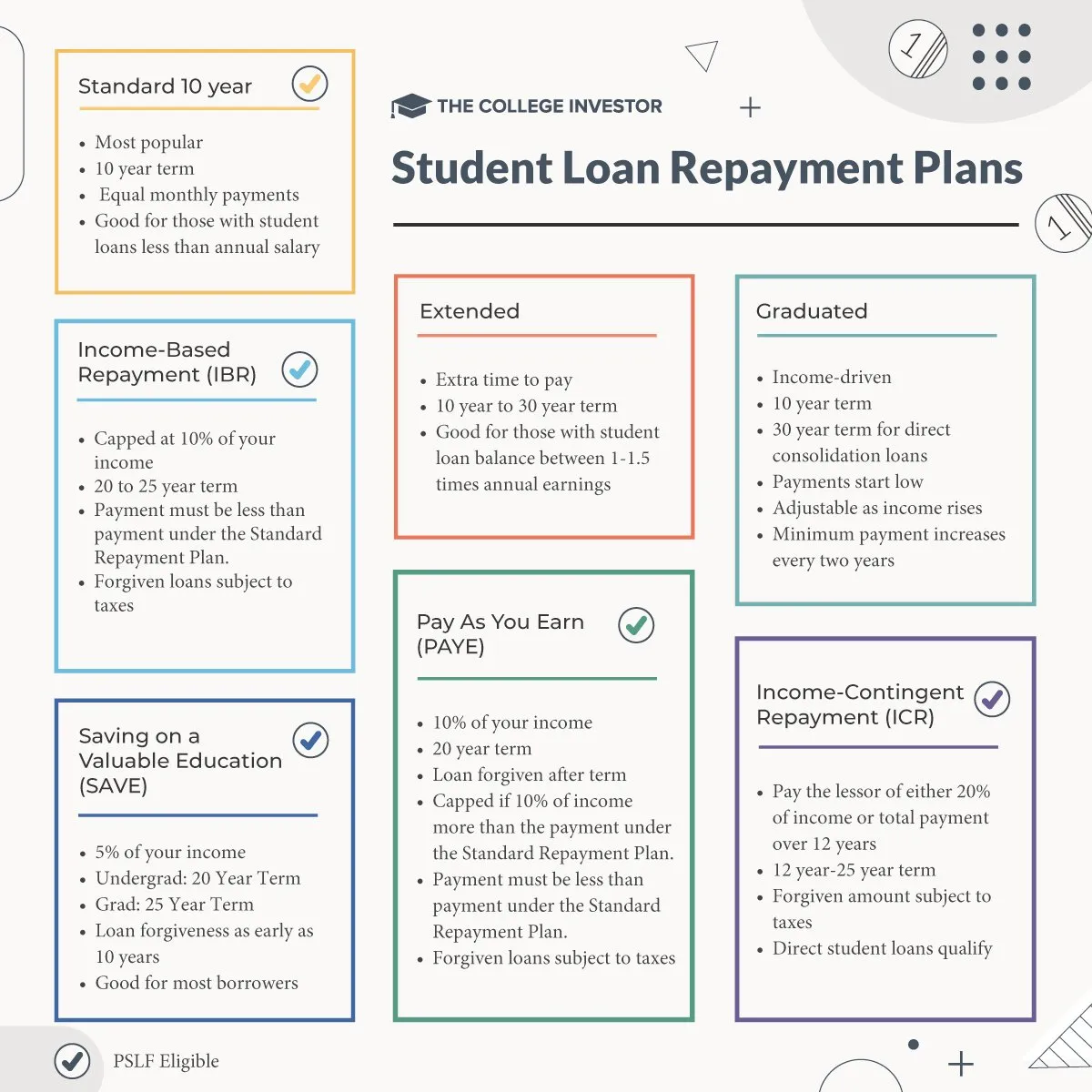

Exploring Repayment Options for Student Loans

When it comes to paying off your student loans, there are several repayment options available to help make the process easier on your wallet. Exploring these options can help you choose the one that best fits your financial situation and goals. Below are some common repayment options to consider:

1. Standard Repayment Plan: This is the default repayment plan for federal student loans. With this plan, you will make fixed monthly payments over a period of 10 years. This plan typically results in the lowest overall interest cost, but your monthly payments will be higher compared to other plans.

2. Graduated Repayment Plan: Under this plan, your payments start out low and increase every two years. This can be a good option if you expect your income to increase over time. However, keep in mind that you may end up paying more in interest over the life of the loan compared to the standard plan.

3. Income-Driven Repayment Plans: These plans base your monthly payments on your income and family size. There are several types of income-driven repayment plans, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), Income-Contingent Repayment (ICR), and Revised Pay As You Earn (REPAYE). These plans can be a great option if you have a low income or high debt relative to your income. They also offer loan forgiveness after a certain number of years of making payments.

4. Extended Repayment Plan: This plan allows you to extend the repayment period beyond the standard 10 years, resulting in lower monthly payments. You can choose to extend the repayment period up to 25 years, depending on the total amount of your federal student loans. While this can make your payments more manageable, keep in mind that you may end up paying more in interest over the life of the loan compared to the standard plan.

5. Refinancing and Consolidation: If you have multiple student loans, you may want to consider refinancing or consolidating them into a single loan with a new repayment term and interest rate. This can simplify your payments and potentially lower your interest rate, saving you money over time. However, be sure to carefully compare the terms of your current loans with the new loan to ensure that you are getting a better deal.

Before choosing a repayment plan, carefully assess your financial situation, including your income, expenses, and future goals. It’s also a good idea to consult with a financial advisor or student loan counselor to help you make an informed decision. By exploring your options and choosing the right repayment plan for your needs, you can successfully pay off your student loans and move forward with your financial goals.

Tips for Shopping Around and Finding the Best Student Loan Deal

When it comes to financing your education, finding the best student loan deal is essential. With so many options available, it can be overwhelming to choose the right one. Here are some tips to help you navigate the process and find the best student loan deal for your needs:

1. Start by researching different lenders and loan options. Don’t just go with the first lender you come across. Take the time to compare interest rates, terms, and repayment options from multiple lenders to find the best deal for you. Look for lenders that offer competitive rates and flexible repayment options.

2. Consider federal student loans before private loans. Federal student loans typically have lower interest rates and more flexible repayment options than private loans. Plus, they don’t require a credit check or a cosigner, making them a great option for many students.

3. Check your credit score before applying for a loan. Your credit score can impact the interest rate you receive on a loan. If your credit score is low, consider taking steps to improve it before applying for a loan. This can help you qualify for a lower interest rate and save you money over the life of the loan.

4. Look for loans with flexible repayment options. Some lenders offer options such as income-driven repayment plans, which allow you to make payments based on your income. This can be a great option if you expect your income to fluctuate or if you’re pursuing a career that may not have a high starting salary.

5. Don’t forget to consider loan servicers when shopping for student loans. Loan servicers are companies that handle the billing and other services on your loan. It’s important to choose a loan servicer that offers good customer service and easy-to-use online tools. Some loan servicers also offer benefits such as interest rate discounts or loan forgiveness programs, so be sure to research your options before choosing a loan servicer.

By following these tips and taking the time to compare different loan options, you can find the best student loan deal for your needs. Remember to borrow only what you need and to carefully consider the terms and conditions of the loan before signing on the dotted line. With a little research and planning, you can finance your education in a way that makes sense for you.